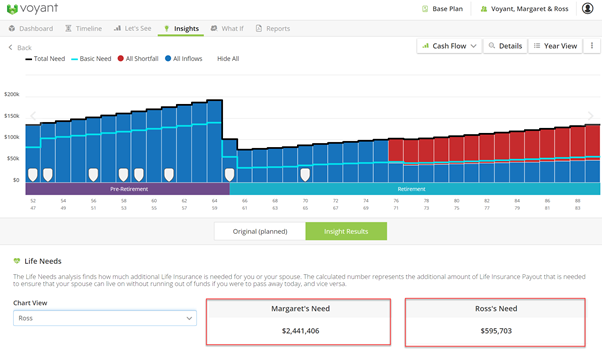

The Life Insurance Need Analysis is used to calculate the lump sum amount required to eliminate any expense shortfall that may occur in a plan following the death of either the primary client and the client’s spouse or partner. It is intended to show as a figure any life insurance coverage shortfall a person may have at the beginning of the second year in the timeline, in order to evaluate how much additional cover that person may want to consider.

In plans for couples, the analyser will evaluate the possible additional life insurance cover needed for the primary client as well as that person's spouse or partner. A simulation will always be run for both persons.

In the year death, which is assumed to be at the start of the second year in the plan, the simulation will add a simulation mortality event and does everything the software would normally do if the specified person were to die at a given point in the planning timeline:

- Benefit payouts are made from active insurance policies.

- If the individual is actively employed at time of death and has death in service coverage provide by an employer, a lump sum payout will be made to the beneficiary. Payments from widow's pensions will also start being paid to the survivor.

- The deceased's estate is currently assumed to be distributed by default to the surviving spouse/partner.

- Property/assets will pass to the surviving spouse/partner.

- Employment and other income earned by the deceased will end

- Expenses, if owned solely by the deceased, will end at mortality.

As with the other insights, you can view the redistribution of assets, payouts from insurance policies and other death benefits, and the adjustment of expenditures (if applicable) while using Life Needs simulation either by clicking the chart details button (top right) and using the slider at the top of the screen to select the year of death or by simply double clicking the second bar/year of the Let's See chart, which will be the year in which the death is assumed to occur – death is assumed to occur at the beginning of the second year in the plan.

Whose mortality-related details are shown will depend on the chart view selected bottom-left when running the simulation. You can switch views easily between the primary client and the client’s spouse or partner.

Expense reductions following mortality

If an expense is co-owned it will continue in the plan at previously set levels. We make no assumptions about which expense should decrease since a plan might contain a mix of expenses, some of which might not be decreased. One's mortgage payment, for example, would not decrease whereas one's living expenses, in general, probably would.

If expense reductions are a concern, consider dividing between client and spouse any expenses that should be reduced automatically upon mortality. Indicate that these are personal expenses by selecting only one owner in the People panel to the right side of the screen. If the owner of the expense dies, that person's personal expenses will also end in the plan.

Once these liquidations and transactions are completed, the Life Insurance Need insight simply runs a lump sum need analysis determine how much would be needed as a lump sum inflow at the selected mortality event in order to prevent any shortfalls from happening afterwards in the cash flow.

Note that the chart only displays a visual of the potential problem, the possible shortfall following death. It does not show the resolution, as is the case with the other need analysers. As a result, you cannot view where the additional lump sum - the result of the need analysis - is being deposited.

What Does the Software Assume is Done with the Lump Sum Inflow?

Any lump sum payouts to the survivor are deposited into the survivor's default cash account - e.g. John's Cash.

Each person in the plan has a default cash accounts (e.g. John's Cash, June's Cash). These notional accounts are used to capture lump sum inflows that are not scheduled to be deposited to specific accounts such as savings, investments or money purchases. Funds deposited into default cash are always used as the first source for top-up income when other inflows have been exhausted and planned expenditures remain unfulfilled.

Funds deposited into default cash accounts or often grown using the default growth rate for cash/savings, which is set in Dashboard view > Plan Settings > Inflation / Growth > Savings Growth Rate.