Plan Settings are the underlying default assumptions used by the software when calculating client cases. In Voyant we code for what we know -- i.e. what the government has announced or legislated -- and when moving beyond the known, we give you, the adviser or paraplanner, tools to set whatever you deem to be reasonable assumptions about future projections.

Note that the assumptions which come packaged with Voyant are just placeholders and are not updated by us, other than changes that relate to legislation. We recommend that you review and decide what assumptions should be used as a firm, prior to use.

System settings which serve as a template of default values for future client cases can only be set in if your firm has a white labelled version of the software. If your subscription doesn't have a white label, client cases created in AdviserGo will initially use the Voyant default assumptions. These can be edited in Plan Settings.

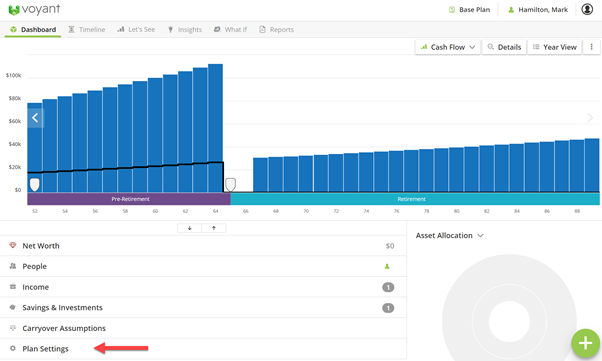

View and edit plan settings in AdviserGo

Editable preferences (assumptions) are found in AdviserGo on the Dashboard screen under the heading Plan Settings.

Plan Settings apply only to the client case at hand and can be changed, if necessary, on a per-scenario basis. The same rules of inheritance from the Base Plan apply.

There are a few deliberate omissions, such as Market Assumptions, default Asset Allocation, and the default settings for the Major Market Loss simulation. These will likely be added to AdviserGo sometime in the future.

Firms that use our rebranding services to manage their preferences can effectively manage the default Plan Settings in AdviserGo as well. The same System Preferences controlled through their rebrand will show as the initial default Plan Settings in AdviserGo, provided they haven’t been edited at some point by the user.

Master list of Plan Settings in AdviserGo

In this list is a summary of how each preference, setting, or option is used in the software.

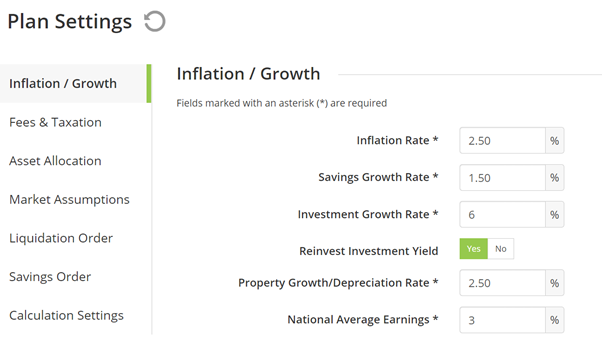

Inflation / Growth

Inflation Rate % is used to inflate expenses and the future purchase price of properties. Importantly, the default inflation rate is also applied whenever a “Present Value” is used. The inflation rate is used to compute the future value of any monetary amount found in the Steps sections throughout the plan input screens. This default can be overridden at the individual item level.

Savings Growth Rate % is used as the default interest rate (Growth Rate) for cash accounts, which are found on the Savings screen. This default interest rate is used provided that Grow this account by Portfolio option is not selected for the account. Importantly, this preference sets the initial default interest rate for the software's Cash Sweep Account (e.g. John's Cash). This default can be overridden at the individual item level.

Investment Growth Rate % is used to set the default growth rate (capital growth) on investments, money purchases and drawdown pensions, provided that Grow this account by Portfolio is not selected for the account. This preference is also used as the default growth rate applied to the hypothetical taxable savings account created when running the Annual Savings Insight. This default can be overridden at the individual item level.

Reinvest Investment Yield allows the yield on investments to be defaulted to either reinvest or pay out annually. Voyant is usually set, by default, to reinvest yields rather than pay them out annually, but this can be easily changed either at the default/plan setting level or on an individual item basis.

Property Growth/Depreciation Rate % is the initial, default rate at which a property, once purchased, will increase or decrease in value. A negative value could be entered in cases where a depreciation rate is deemed appropriate. For a future property purchase, the Inflation Rate is used to compute the future value of a property when purchased. This default can be overridden at the individual property level.

National Average Earnings % is used as the default rate of income inflation for Employment and Other Income. This default can be overridden at the individual item level. It is also used to increase the Superannuation contribution limits.

Annuity Assumed Interest Rate % is used as the default annuity interest rate, which is used to convert an accumulated pension fund into an annuity or to calculate payments when purchasing any future annuity. This default can be overridden at the individual item level.

RPI % the Retail Price Index can be used (if selected) to inflate items such as escalating final salary pension and annuity payouts.

Default Tax Table Assumption % can be used to edit and apply an across-the-board annual escalation to the future tax related assumptions such as tax brackets.

Centrelink COLA Rate % is the percentage the Age Pension maximum benefit amount will increase by each year. It also increases the thresholds for the income and assets Age Pension tests.

Pension COLA Rate % increases the value of the Superannuation Transfer Cap.

Fees & Taxation

Default Fees % A list of account types is available in this section allowing you to set a default rate of fees based on account type. Fees, if applicable, are deducted from capital growth.

Account Liquidation Annually % sets the default for the Capital Gains Realised Annually field, an option available for some taxable investments, such as unwrapped investments, in the Growth data input section.

Liquidation Order

The liquidation order is used to set a default order for asset liquidation based on asset type. Read more >>

Savings Order

The savings order is used to set which types of accounts receive priority when multiple contributions are set to occur in a given year. Read more >>

Calculation Settings

Transfer all excess income/credits to savings is usually set to No by default as Voyant is normally set to assume unallocated surplus is spent. You have the option, however, to switch this setting to Yes and assume the opposite. Use this setting to assume leftover surplus is saved, if you think this approach is appropriate for your clients and their lifestyle. Read more >>

Save income after retirement as with the above setting, is usually set to No by default as Voyant is normally sets to assume unallocated surplus is spent. Switching this setting to Yes allows you to assume that surplus is saved in the retirement stage. Prior to retirement, surplus will be assumed spent. Read more >>

Grow all investment and retirement accounts using asset allocation is usually set to No by default. Switching this setting to Yes automatically sets all investments and retirement accounts to be grown using asset allocations. Note that when this is set to No you have the option to grow accounts using either a fixed growth rate or to have growth derived from an asset allocation. When this setting is set to Yes the Grow this account by dropdown will be set to Portfolio/Holdings in the Growth section of the input screens and cannot be changed to Entered Capital Gains and Yield.

Grow all savings and cash accounts using a 100% cash allocation is usually set to No by default. Switching this setting to Yes automatically sets all savings accounts to be grown using a 100% cash asset allocation. Note that when this is set to No you have the option to grow accounts using either a fixed interest rate or to have growth derived from a 100% cash asset allocation. When this setting is set to Yes the Grow this account by dropdown will be set to Portfolio/Holdings in the Growth section of the input screens and cannot be changed to Entered Interest Rate.

Overriding Plan Settings - Editing assumptions at the item level within a plan

The default growth rates and other assumptions, found on the Plan Settings screen will be used as the initial default values when creating a client case. However, most these defaults can be overridden, when necessary, by making edits at the item level.

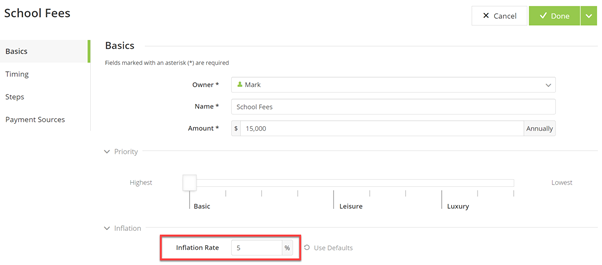

For example, the default Inflation Rate for all expenses in the plan could be set to 2.5% in the Plan Settings. This means whenever a new expense is added to the plan, that expense will be set to inflate in the future at a rate of 2.5% per annum.

However, perhaps there is a particular expense, education or health care costs for example, that should inflate more rapidly. Exceptions to the default can be made by simply editing the Inflation Rate for that expense individually.

Any edits made at the item level will override the initial defaults from Plan Settings. Moreover, once edited at the item level, these settings will remain as edited for the item, regardless of any later changes made in Plan Settings.

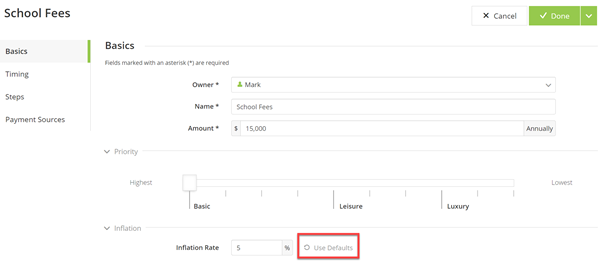

How to revert a setting edited at the item level back to the Plan Settings

Should you ever need to revert a setting edited at the item level back to the plan default, click Use Defaults and the item will once again use the default value taken from Plan Settings.

Outputting Plan Settings in printable reports

Information about the software's Plan Settings can also be output in printable pdf reports. Reports can be generated from the Reports screen. For more information on how to generate a report click here.

The main AdviserGo report that relates to plan settings is the Assumptions report. This report contains most of the client-facing values from the Plan Settings that would be meaningful to your client. It is not intended to include all of the software's preferences. Rather, the report only features preferences that have an obvious bearing on your client's plan.

The Financial Summary report also has a summary of a the main inflation and growth assumptions. Click here for more information on this report.