Which assets will Voyant access to pay expenses?

AdviserGo will work out most of the future cash flow for you, if you let it. If annual income doesn’t fully meet planned expenses, the software will automatically top-up income from liquid assets in order to prevent potential shortfalls in the cash flow, provided you place no Liquidation Limits on these accounts.

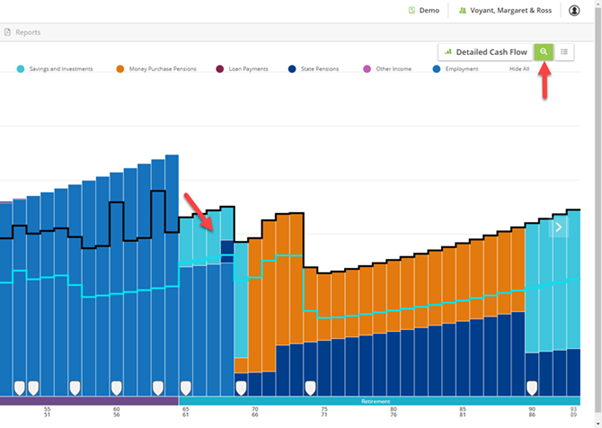

You can see these assets being used rather than income in many cases by clicking the detailed view of the Cash Flow chart via the magnifying glass icon. The black need line represents your client’s total annual taxes, expenditure, and any planned savings and investments that are being met successfully in that year of the plan. By default Voyant withdrawals from liquid assets, such as Savings and Investments, to conveniently meet the top of the black need line.

Liquid assets include savings, investments, and after retirement, various retirement savings accounts.

Illiquid assets, those entered on the Property/Assets screen, are never liquidated automatically.

Goals and expenses are fulfilled in order based on priority

Goals and expenses are fulfilled based on their priority. As may be the case at some point in a long-term cash flow projection, numerous planned goals and expenses may be in competition for finite resources. If the income and assets available at a given point in time are insufficient to completely fulfill one’s planned expenses and goals, the cashflow problem will be noted with a red shortfall in the Cash Flow chart.

As the software determines which goals and expenses will be fulfilled, it will work through Basics first, starting with the highest priority basics, before moving through the lower-level basics. The software will then attempt to fulfill the three levels of Leisure expenditures, in order, before moving down through the three levels of Luxury expenditures.

Contributions and some expenses, such as taxes, debt payments and insurance premiums, are generated automatically by the software. The priorities of these expenses are assigned automatically by the software and cannot be edited. Contributions and auto-generated expenses are worked into expense fulfilment in the following order.

1. Pre-tax contributions are made, usually to retirement savings. Also, contributions are made that have been specially set to be made before paying expenses – e.g. using the “contribute before paying expenses” setting.

2. Taxes and other government withholdings are taken from income.

3. Secured debt payments (debts linked to properties) are made. Secured debts are those which you link to a property/asset in the software.

4. Unsecured debt payments are made. Unsecured debts, such as credit cards or an unsecured loan, are those not linked to any property/assert in the software.

5. Insurance premiums are paid. Insurance premiums are expenses created automatically by the software when you enter an insurance policy into a plan.

6. Basic expenses and goals are fulfilled in order based on their user-assigned priority level. These are expenses and goals assigned to priority levels 1-4 using the prioritisation slider (pictured below).

7. Future asset purchases are made.

8. Leisure expenses and goals are fulfilled in order based on their user-assigned priority level. These are expenses and goals assigned to priority levels 5-7 using the prioritisation slider.

9. Annuity purchases are made.

10. Luxury expenses and goals are fulfilled in order based on their user-assigned priority level. These are expenses and goals assigned to priority levels 8-10 using the prioritisation slider.

11. Regularly scheduled contributions are made to savings, investments, and in some cases to retirement accounts that accept post-tax contributions. Contributions at this stage are prioritised in part based on general category or possibly the specific type of account, using the Savings Order setting in Plan Preferences.

How are expenses fulfilled?

Expense fulfilment is a complex aspect of the software. In this section we will show you how the software works out the cash flow and how you might control it. The software does offer some high-level control over the order in which accounts are liquidated via the Liquidation Order (explained below). Beyond this, withdrawals can be controlled, if necessary, by setting Withdrawal Limits, Transfers and/or Planned Withdrawal strategies on individual accounts. We will show you how to do this in a moment. Otherwise, simply leave the software to work out the cash flow for you.

Expenses are always met in the following order via four distinct stages:

1. Expenses are first fulfilled from income / credits. This includes income from the minimum annual payment from Supers. The software will automatically calculate the minimum amount and add this to the plan

2. If expenses remain, draws are made from ready cash accumulated in the default cash accounts (John's Cash and Julia's Cash).

3. If expenses remain, draws are made from other cash accounts such as current and savings accounts (accounts entered into the plan under the Savings Type).

4. If income and ready cash are not sufficient to meet expenses, funds will be drawn from available liquid assets (i.e. the Plan Settings - Liquidation order as explained below).

Note - Preferred payment sources for certain types expenses and goals and Withdrawal Limits on accounts can override these stages.

Within each of these five distinct stages, the software checks for ownership and attempts to fulfil the expense first according to the person (or persons) who own it. For example, if an expense is owned by Paul, Paul's funds will be used first before moving to jointly owned accounts and then to his wife Cathryn's accounts.

Once the software reaches stage 4 of expense fulfilment, the Liquidation Order setting comes into play. Located in Plan Settings, the Liquidation Order setting allows you to specify a category-based order in which the expense owner's liquid assets will be liquidated.

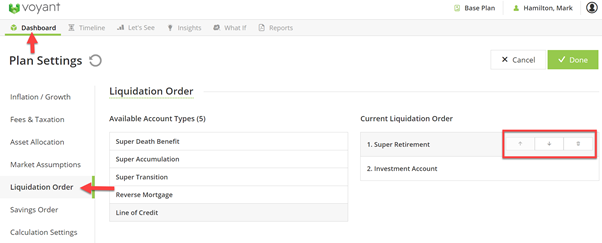

Plan Settings – Setting the asset liquidation order

The order in which assets are liquidated can be set at a very general level, by asset category, in Plan Settings > Liquidation Order. Plan Settings can be found on the Dashboard.

The default liquidation order, which can be changed, is normally Super Retirement first, then Investment Account.

To change the high level Liquidation Order click on the category you want to move in the Current Liquidation Order column and use the arrows to move it up or down the list.

The Available Account Types in the left column allow for product-specific account types to be added and positioned among the broader asset categories. For example, if the strategy is to liquidate Super Transition before Super Accumulation, these two types of accounts could be added to the liquidation order to the right and positioned accordingly.

Cash accounts are a category of accounts not shown in the Liquidation Order. These accounts are intentionally excluded from the Liquidation Order because they are usually liquidated prior to the types of accounts shown in the liquidation order. Cash accounts include:

- The notional, default Cash Sweep Accounts created by the software for each person in the plan (e.g. John’s Cash, Julia’s Cash),

- Current and Savings accounts.

Withdrawal limits can be used to override the expense fulfilment Order

Withdrawal Limits can also trump the normal expense fulfilment order. If you limit or disallow the software from taking ad-hoc withdrawals from a savings account or investment, that account will be effectively removed from or limited in the expense fulfilment process.

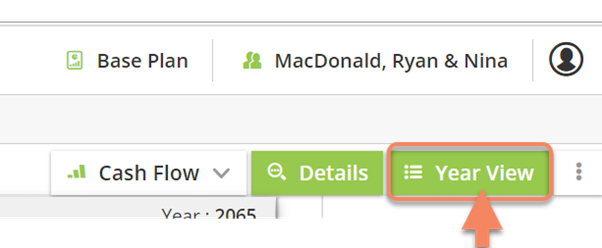

Where can I see what withdrawals are happening?

Further details about withdrawals can be viewed by double clicking any bar/year of the chart or by clicking the Year View button, top-right.

Choose the Investments tab to see withdrawals from Savings and Investments or the Pensions/Retirement tab to see withdrawals from pensions/retirement accounts. Use the scroll bar to see different years.