Income from self-employment is set on the Employment screen, by selecting an Income Source of Self Employed.

Unlike employed individuals and company owners, self-employed individuals are not assumed to pay tax via PAYE. Instead, they pay income tax at assessment, in the subsequent year of the plan. They are also subject to Class 2 and, possibly, Class 4 National Insurance tax rates also.

In plans with self-employed individuals, there would likely be a tax bill coming due in the first year of the plan. The software has no way of deducing what your client's earnings were in the year prior to the plan. Therefore, be sure to enter these carryover taxes – and for that matter other allowances that may need to be carried over from the plan’s prehistory – on the Carryover Assumptions screen.

Where to enter taxes due from self-employment

Since self-employed individuals do not generally pay taxes via pay-as-you-earn (PAYE), the software assumes their taxes are paid at assessment in the following year of the plan.

Taxes on self-employment income from the first year of the plan would therefore be paid in the second year of the plan and so on.

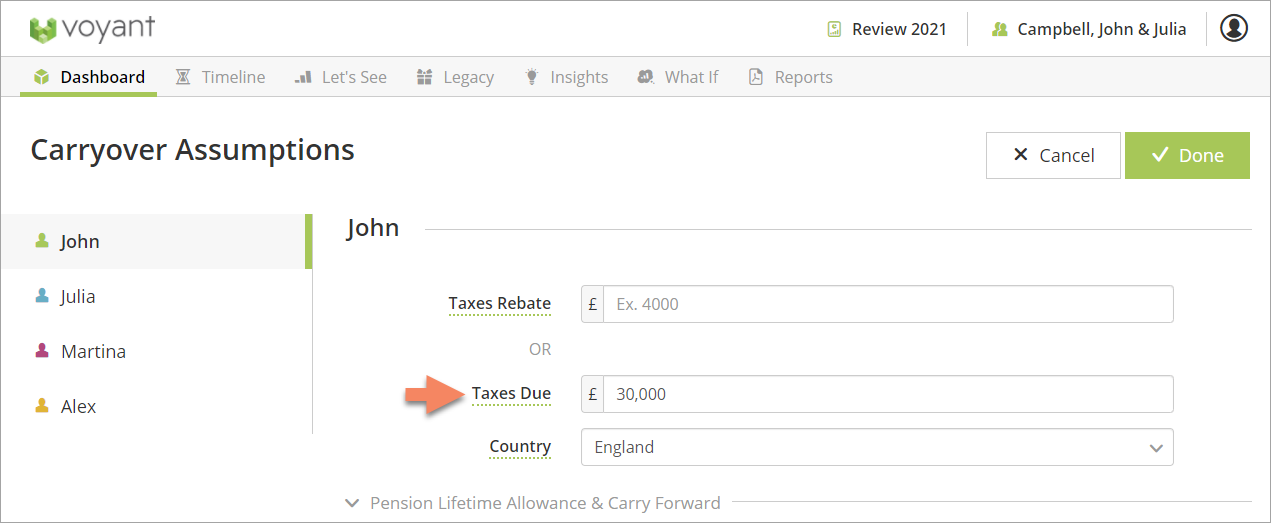

To capture any taxes due on self-employment income from the year prior to the plan's start, go to the Dashboard screen and select the Carryover Assumptions link, one of the bottom two links in the middle of the screen. Select the name of the earner to the left of the screen. Enter these taxes due from the year prior to the start of the plan in the Taxes Due field.

These taxes due will then appear as a first-year expense in the Cash Flow chart.

Related topics

Taxes for self-employed individuals in the first year of the plan