Standard Fund Threshold (SFT)

The software is hard-coded with the legislated Standard Fund Threshold increases:

2025: €2m

2026: €2.2m

2027: €2.4m

2028: €2.6m

2029: €2.8m

Thereafter, the SFT increases by the Standard Fund Threshold Escalation Rate found in Plan Settings > Inflation/Growth:

Tip - to keep the Standard Fund Threshold level at €2.8m from 2029 onwards set the Standard Fund Threshold Escalation Rate to 0%.

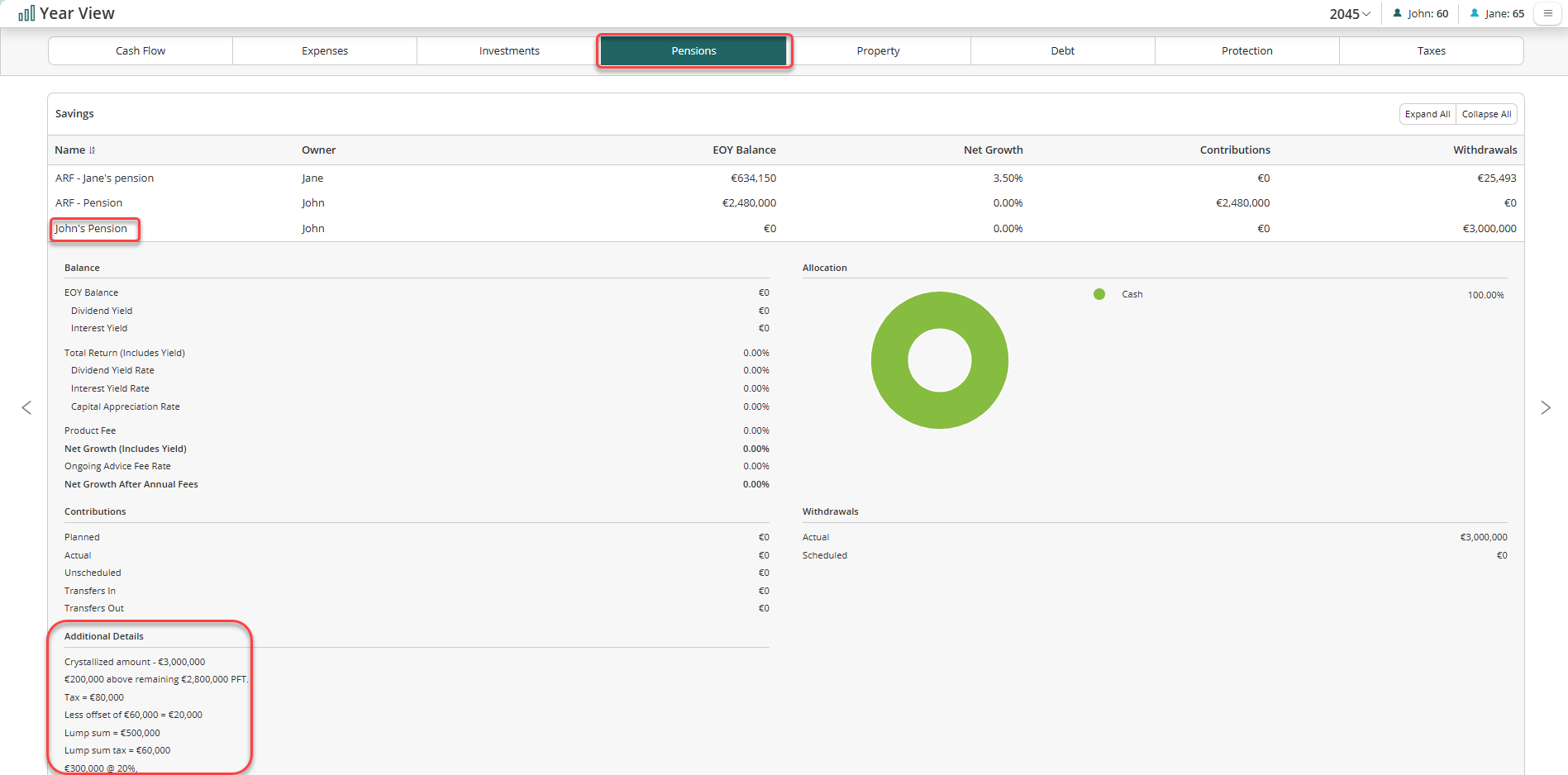

The amount of Standard Fund Threshold in any particular year isn't displayed on screen. What can be seen is the remaining Standard Fund Threshold in any year in which the crystallised amount exceeds the remaining SFT.

To view this, click Year View > Pensions for the year of the crystallisation, then click on the pension being crystallised to expand additional detail:

Personal Fund Threshold (PFT)

If the client is entitled to a higher threshold because their pension fund was over €2m on 1 January 2014, it is possible to reflect their Personal Fund Threshold in their plan.

To do this, go to Carryover Assumptions > Personal Fund Threshold & Lump Sum and input the amount of their PFT in Protection Amount:

Tip - the software will use the higher of the Personal Fund Threshold (Protection Amount) or the Standard Fund Threshold in the year of crystallisation. For example, if the client's PFT is €2.5m and their pension is crystallised in 2026 when the SFT is €2.2m, the PFT will be used. However, if the crystallisation is in 2029, when the SFT is €2.8m, the SFT will be used.

SFT/PFT usage which pre-dates the start date of the plan

If the client has used part of their SFT/PFT prior to the start date of the plan, this can be reflected in Carryover Assumptions > Personal Fund Threshold & Lump Sum. Input the percentage already used in Percent of Threshold Used. Lump sums taken from pensions prior to the start date of the plan can be reflected in the Previous Lump Sum Amount field.

For example, if the client used €500,000 of their SFT when the SFT was €2,000,000 and they took a lump sum of €125,000, the Percent of Threshold Used would be 25% and the Previous Lump Sum Amount would be €125,000:

Based on the above example, the next time there is a crystallisation in the plan, the remaining SFT will be 75% of whatever the SFT is at that point in time e.g. if the SFT is €2,200,000, the remaining SFT will be 75% x 2,200,000 (1,650,000) not 2,200,000 - 500,000 (1,700,000).

Tip - the software calculates and records the SFT/PFT usage in the background for crystallisations which occur during the plan's timeline.