Pension splitting allows a spouse to give up to 50% of their eligible pension income to their spouse for tax purposes only. Pension splitting doesn’t involve an actual transfer of funds between accounts within the software, it is a paper transfer shown in the tax section of your plan.

What is eligible pension income?

The most common form of “eligible” pension income is income from a registered company pension plan whether it is a defined benefit pension or defined contribution pension.

Individuals who do not have a registered workplace pension plan can still take advantage of pension splitting once they convert their RRSPs or deferred profit-sharing plans into income through a life annuity or a RRIF.

Income from the Canada Pension Plan (CPP) and Old Age Security (OAS) do not qualify as eligible pension splitting. However, CPP has its own set of rules for CPP splitting (sharing).

You must be married or in a common-law partnership with each other in the year.

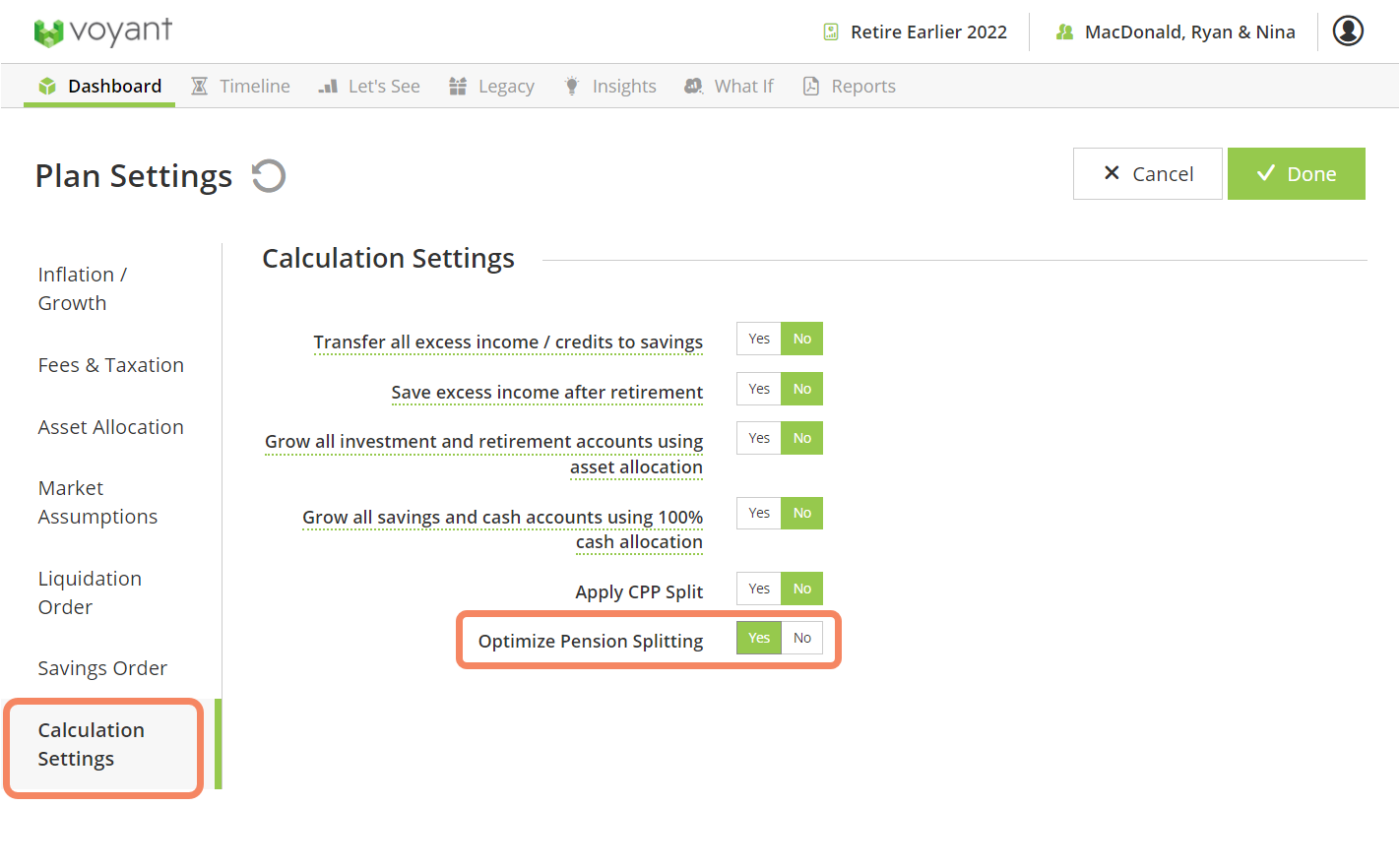

How do I tell the software to split the pension income?

To optimize pension splitting within your plan, go to Plan Settings and select the Calculation Settings section. Select "yes" on the "Optimize Pension Splitting" setting.

How will this affect my plan?

The screen shot below is from the tax section in a year where there was a withdrawal from one of the spouse's pension accounts. The section provides a breakdown of how they are arriving at the taxable income.

In this example we see Ryan's initial pension withdrawal of $105,311 being split and half added to his spouse Nina's spouses taxable income.

In contrast here is the view of the same year in the same plan when the "optimize pension splitting" setting is set to "no".